Geopolitical issues remained the center of attention during 1Q26.

During the first quarter, geopolitics dominated the global landscape. The United States played a leading role through several key actions: it intervened militarily in Venezuela to facilitate a change in leadership and strengthen control over oil; it showed interest in Greenland, generating tensions with the EU but ultimately reaching an agreement that boosts Europe’s strategic autonomy.

Likewise, the United States and Israel launched a large-scale offensive against Iran with the aim of dismantling the country’s military and nuclear capabilities and forcing a regime change. Iran responded by closing the Strait of Hormuz. It also carried out attacks against Israel, against U.S. bases in the region, and against energy infrastructure in Persian Gulf countries. Subsequently, the United States and Iran agreed to a two-week ceasefire. The Trump administration expressed its dissatisfaction with the lack of support from several European partners in this conflict and threatened the withdrawal of the United States from NATO.

The offensive against Iran triggered a notable reaction in financial markets, with a significant increase in global oil prices and in natural gas prices in Europe, leading to a rise in market inflation expectations in Europe.

At the same time, there was an upward recalibration of expectations for the future path of central bank interest rates.

• For the ECB, markets came to price in three rate hikes this year (before the conflict, rate stability had been expected). This also caused a sharp rise in interbank rates, with the 12-month Euribor reaching highs not seen since 2024. ECB members have generally shown caution in response to the rebound in oil prices, although some have left the door open to a rate hike in April.

• For the Fed, markets are pricing in rate stability. Prior to the conflict, expectations had included slightly more than two rate cuts for this year.

In this context, government bond yields rose on both sides of the Atlantic.

The euro depreciated against the dollar due to the impact of the energy shock in Europe, following the appreciation it experienced prior to the outbreak of the conflict, when it surpassed USD 1.20 per euro.

Meanwhile, even before the outbreak of the conflict in the Middle East, relevant dynamics had already been observed in financial markets linked to the development of artificial intelligence. The technology sector had shown relatively weaker performance amid growing concerns over upward revisions to capital expenditure (capex) investment plans by major tech companies. At the same time, the emergence of increasingly advanced AI models fueled fears of structural disruptions—especially in the labor market—which translated into stock market declines across several sectors. The software sector was particularly affected.

These tensions also spilled over into private markets, due to their high exposure to the technology sector and, in particular, to software. Indeed, several private credit funds were forced to implement withdrawal restrictions following a sharp increase in redemption requests from retail investors.

Uncertainty regarding macroeconomic impacts remains high and will depend largely on the duration of disruptions in the energy market.

Additionally, the increase in energy prices has already impacted March inflation data. Inflation in the euro area rose to 2.5% year-on-year, above the ECB’s target, while in Spain it increased to 3.3%. In the United States, inflation rose to 3.3%, its highest level since 2024.

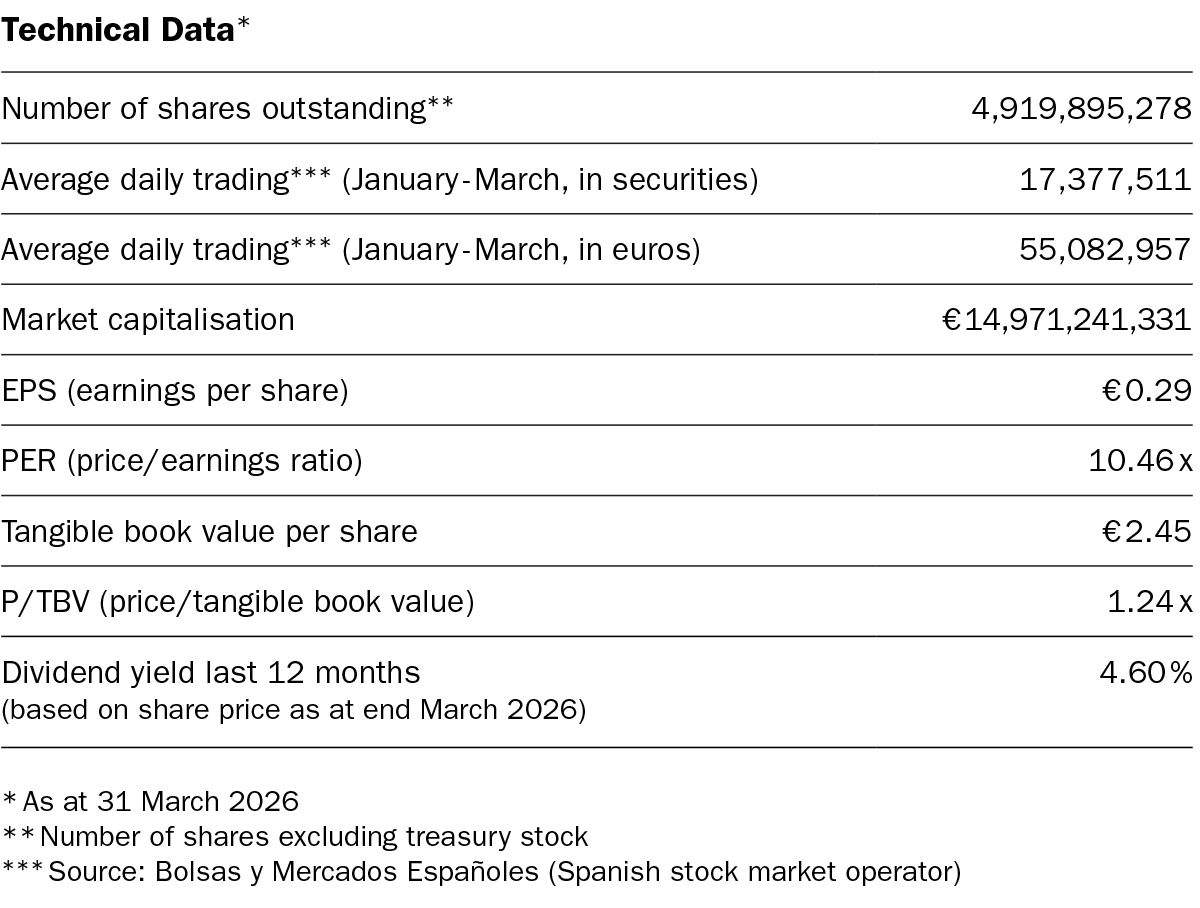

Banco Sabadell carried out its first debt issuance of 2026 in January, consisting of a €500 million issuance of mortgage-covered bonds.

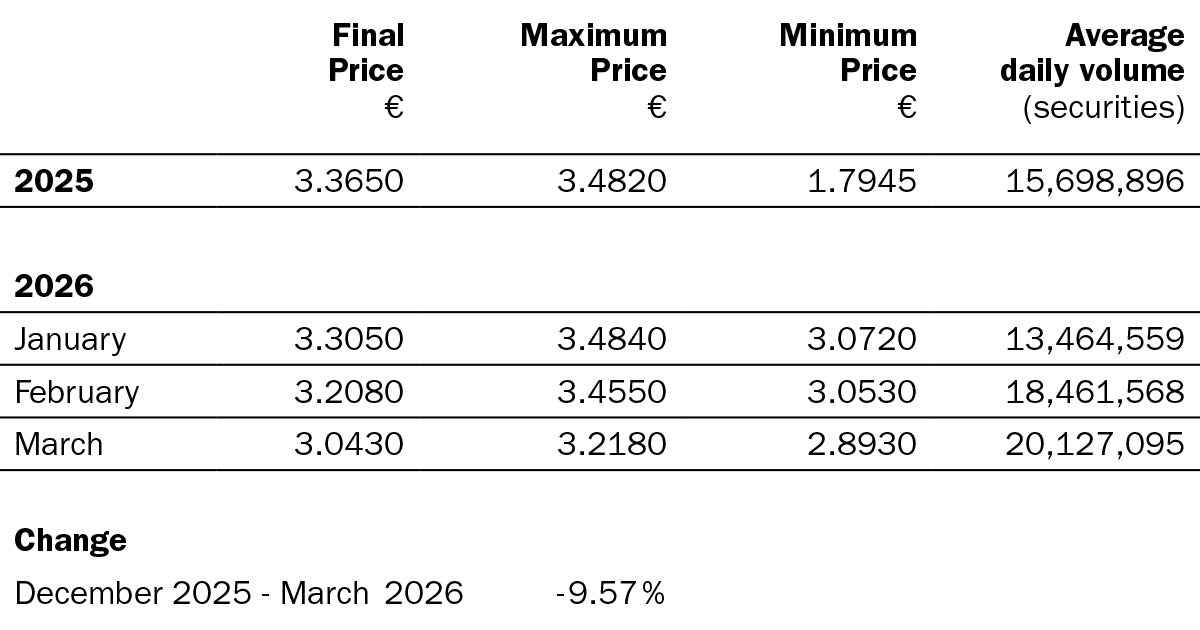

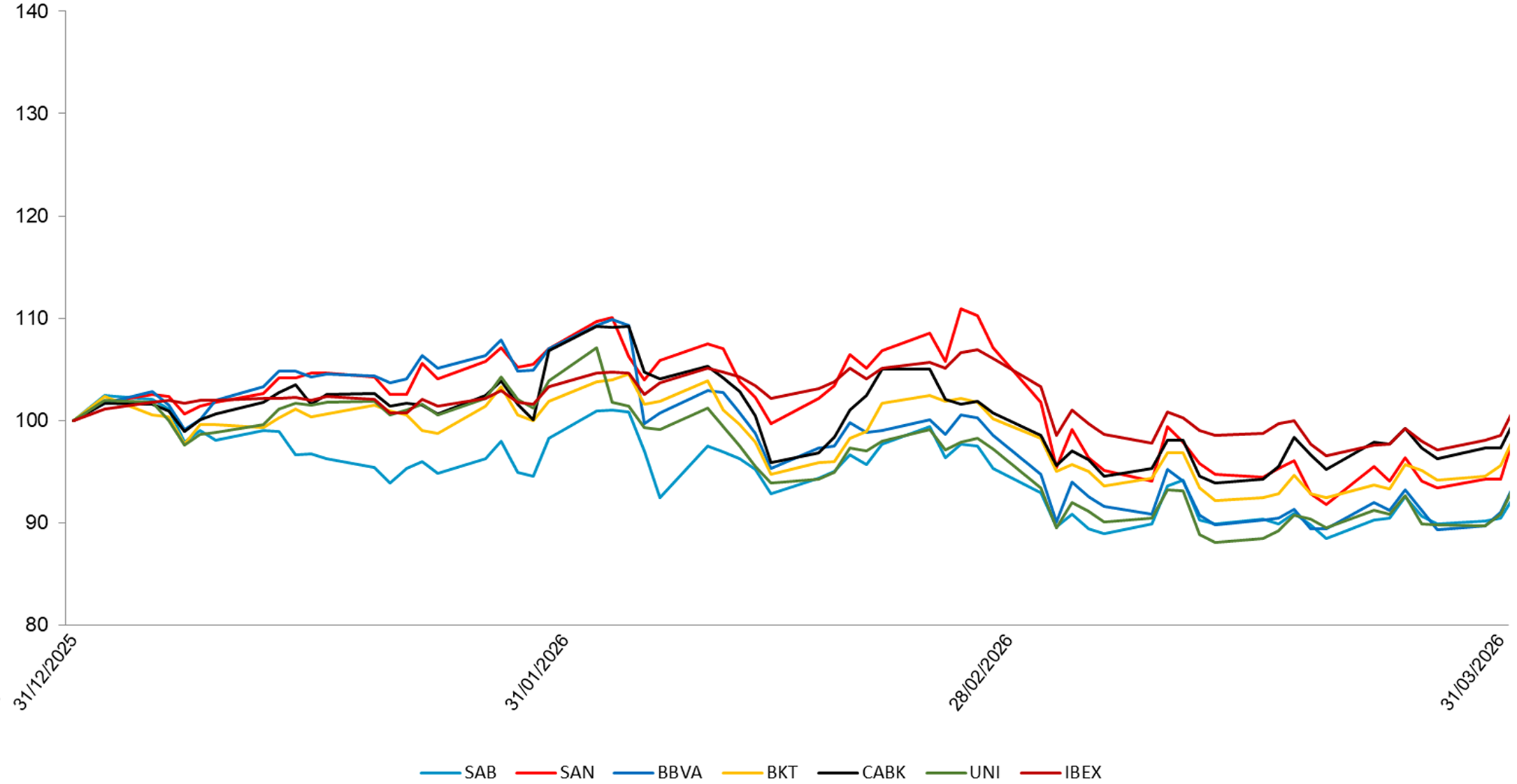

Finally, Sabadell’s share price closed the quarter with a cumulative dividend-adjusted decline of -9.6%, underperforming the average of comparable Spanish banks1 (−5.4%) and the European banking sector (−7.1%).

1. Comparable Spanish banks include CaixaBank, Bankinter, and Unicaja.

*Source: Bolsas y Mercados Españoles (Spanish stock market operator)

Source: Bloomberg. Data rebased to 100 at the start of the period, adjusted for capital increases, dividends, stock splits, etc.

(i) Past performance is no guarantee of future returns.